Has the lockdown party ended for dry bulk?

Jan, 27, 2022 Posted by Gabriel MalheirosWeek 202204

Last year the Baltic Dry Index (BDI) rose nearly threefold from an average of 1,066 in 2020 to an average of 4,948 in 2021. Capesize average earnings (based on the 5TC measure published by the Baltic Exchange) grew from an average of $13,000 in 2020 to $33,100 in 2021. Panamaxes (basis the Baltic’s P4TC average) went from $8,600 in 2020 to $25,400 in 2021, supramaxes from $8,200 to $26,700 and lowly handysizes tripled from $8,000 in 2020 to $25,700 in 2021.

But then, in October, China introduced its steel production cap and its three red lines policy of preventing over-leveraged property developers from borrowing more money. The BDI fell 61% from a peak of 5,647 on October 6 to end the year at 2,217. In January it has continued to fall, averaging just 1,923 points to January 21.

Brokers and operators are blaming the weak market on lockdowns in China, the debottlenecking of ports in China, the Indonesian coal export ban, the easing of the Indonesian export ban, the Winter Olympics, Christmas and the western New Year holidays, a sudden surfeit of ballasters, rains in Brazil, a lack of rain in Brazil and Argentina, and even fog in the Bosporous. In other words, sentiment is almost universally negative but there is no smoking gun, no single cause that everyone can agree on for the fall in the market.

Whatever the reason, key freight routes are plummeting. In the Pacific, the leading capesize round voyage route C5 is down to $6.7 or thereabouts even as iron ore prices have recovered to levels last seen in October last year at the peak of the freight market.

In the Atlantic, the C3 Brazil- China route is down to $17.60 from a peak of $47+ in October. It is back to levels last witnessed in March 2021. Rains in Brazil did cause a hiatus in loading cargo at key iron ore export ports. The rainy season tends to last for much of the first quarter of every year but has been heavier than usual this year.

Presumably, the cargoes will be backlogged rather than lost, if port productivity can be optimized later in the year. As this seasonal effect is annual, Vale appears to be sanguine and has not downgraded its export estimates for the year of the usual 320-350m tonne range.

In the grains markets, hot and dry weather has damaged South American soy and corn crops. The US Department of Agriculture suggests Brazilian soy and corn production is down 8m tonnes from their previous forecasts for this crop year. The Rosario Grain exchange suggests even lower yields.

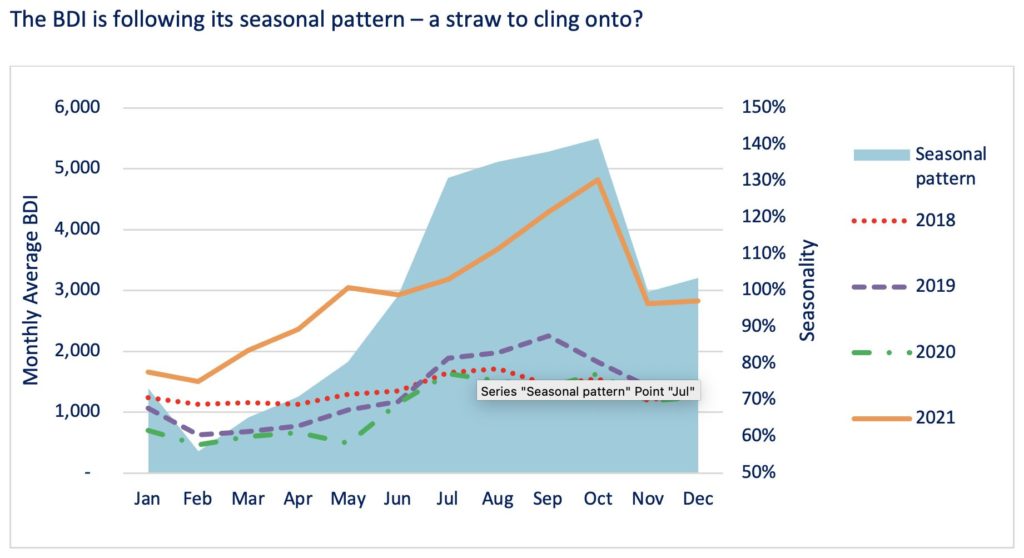

Is this for the current market cycle which began at the start of 2020? There is hope for operators. Earnings were last at these levels a year ago around Lunar New Year 2021. The BDI has followed exactly the seasonal pattern of the last several years by peaking in October and bottoming out around Lunar New Year, before going on a nine-month bull run. If the BDI can average more than 1,658 points this January, it will be ahead of January 2021 already.

Source: Splash247

To read the full original article please visit: https://splash247.com/has-the-lockdown-party-ended-for-dry-bulk/

-

Grains

Aug, 02, 2021

0

Brazil to increase soybean planting for the 15th year, says Datagro

-

Meat

Apr, 29, 2022

0

Increased exports boost poultry meat prices in Brazil; brisket and fillet set new records

-

Trade Regulations

Aug, 07, 2024

0

Ag ministry defines requirements for melon imports to avoid pests

-

Fruit

Sep, 23, 2024

0

Argentine cherry exports poised for growth