New DataLiner data: container trade rises amid persistent pressure on East Coast South America freight rates

Jun, 01, 2026 Posted by Gabriel MalheirosWeek 202623

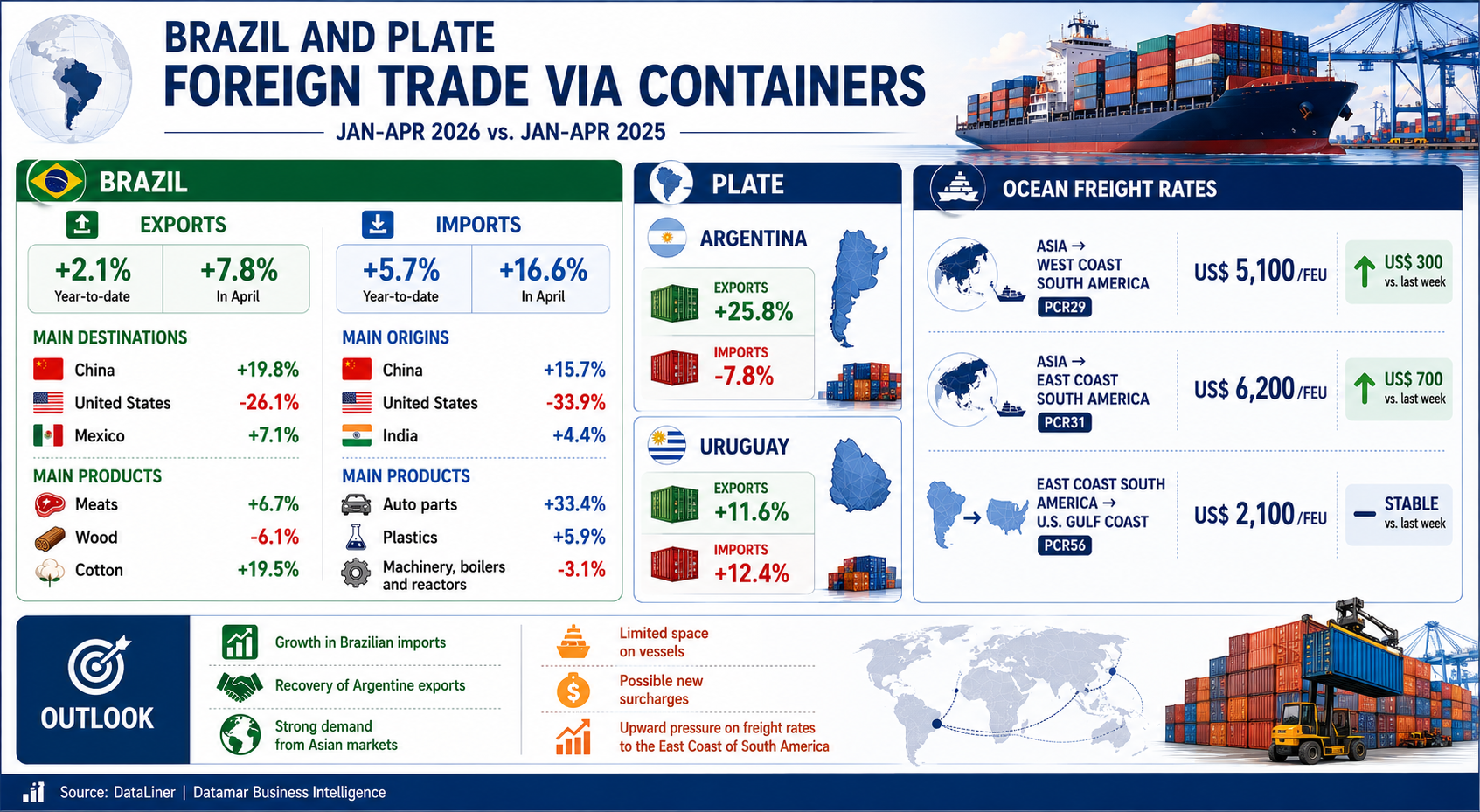

Newly released data from Datamar’s Business Intelligence team on Brazilian container throughput show that Brazilian container exports rose 2.1% from January to April 2026 compared with the same period last year. In April alone, exports grew 7.8% from April 2025. See the chart below:

Brazilian Container Exports

Source: DataLiner (click here to request a demo)

The result comes amid a reshaping of international trade, marked by geopolitical tensions, changes in global supply chains and efforts by exporters and importers to reach new markets. Despite the uncertainties, international demand for food, fibers and raw materials continues to support shipments from South America.

China remained the top destination for Brazilian container exports, with volumes up 19.8% from the first four months of 2025. The United States ranked second, despite a 26.1% drop in shipments, followed by Mexico, where volumes rose 7.1%.

The growth in shipments to China reinforces the importance of the Asian market for Brazilian foreign trade at a time when companies worldwide are seeking to diversify suppliers and trade routes amid geopolitical uncertainty and changes in global trade policies.

Meat was Brazil’s main containerized export commodity from January to April 2026, with volume up 6.7% from the same months of 2025. It was followed by wood, down 6.1%, and cotton, up 19.5%. The performance of meat and cotton reflects international demand for food and raw materials, especially in Asian markets.

Brazilian container imports rose 5.7% in the first four months of 2026 compared with the same period in 2025. In April alone, inbound volumes increased 16.6%. See below:

Brazilian Container Imports

Source: DataLiner (click here to request a demo)

China was the main origin of Brazilian container imports from January to April 2026, with volume up 15.7% from the same months of 2025. It was followed by the United States, where volume fell 33.9%, and India, where volumes increased 4.4%.

The figures show China’s consolidation as Brazil’s main supplier of manufactured goods and reinforce the growing trade integration between the two countries.

Auto parts were Brazil’s top containerized import commodity in the first four months of 2026, with volume up 33.4% from the same period last year. They were followed by plastics, up 5.9%, and reactors, boilers and machinery, down 3.1%. The increase in auto parts imports suggests continued demand from Brazilian industry for imported inputs and components.

Source: DataLiner (click here to request a demo)

River Plate

Argentine container exports rose 25.8% in the first four months of the year compared with the same period in 2025. Imports, in turn, fell 7.8% over the same period.

Argentina’s performance comes amid economic reforms aimed at increasing external competitiveness and stimulating exports, supporting the recovery of the country’s trade flows.

Uruguay recorded an 11.6% increase in container exports and a 12.4% rise in imports from January to April 2026 compared with the same months of 2025, reinforcing its position as an important regional logistics hub.

Freight rates to South America rise

Container freight rates to South America also jumped in the week ended May 29, driven mainly by tighter space availability, according to Platts’ America Container Freight weekly report.

According to freight forwarders heard by Platts, carriers have been creating a kind of “rate peak season” through blank sailings, geopolitical uncertainty and high fuel costs.

On the North Asia-West Coast South America route, PCR29, freight rates rose US$300 during the week to US$5,100 per FEU.

On the North Asia-East Coast South America route, PCR31, rates increased US$700 to US$6,200 per FEU, one of the highest levels recorded in recent months. Available space for shipments in the first week of June became extremely limited because of canceled calls, equipment shortages and operational adjustments by carriers.

CMA CGM announced a peak season surcharge of US$1,000 per FEU starting June 20, while other carriers are expected to adopt similar measures.

On the East Coast South America-U.S. Gulf Coast route, PCR56, freight rates remained stable at US$2,100 per FEU.

Outlook

The outlook for the coming months suggests continued pressure on freight rates to East Coast South America. In addition to the reduction in space supply by carriers, the market is monitoring the effects of tensions in the Middle East, which continue to affect fuel costs and marine insurance, as well as developments in U.S. tariff policies and trade negotiations involving Mercosur.

The Asia-East Coast South America route is expected to remain particularly heated. Growth in Brazilian imports, the recovery in Argentine exports and sustained demand from Asian markets for South American products are likely to keep volumes in the region elevated during the second half of the year.

If vessel and equipment availability remains tight, carriers may implement further rate increases and surcharges. In this context, shippers operating on the East Coast of South America are likely to face higher logistics costs and a greater need for advance cargo planning.

At the same time, the possible implementation of the Mercosur-European Union agreement and progress in other trade negotiations could create new opportunities for exporters in the region in the coming years, further strengthening the strategic importance of East Coast South America in global container routes.

-

Shipping

Aug, 25, 2023

0

Panama Canal Authority warns restrictions will stay in place for at least 10 months

-

Ports and Terminals

Dec, 14, 2020

0

Codeba moves 1 million tons in November

-

Grains

Dec, 08, 2022

0

Taiwan buys 130,000 t of corn from Brazil in private deals

-

Automotive

Oct, 29, 2025

0

Alckmin urges Chinese ambassador to secure chip exports to Brazil as crisis looms